'End this depression now' (Reseña del libro de Paul Krugman)

"End This Depression Now". Autor: Paul Krugman. Editorial: WW Norton and Penguin (Editorial Crítica en la versión española). 1ª edición: 2012. Páginas: 272. Precio: 19 euros en España

Crítica introductoria Know Square

Krugman manifiesta vehementemente que la economía no es un juego moral, pero toda su orientación económica está dirigida por su visión social-demócrata. La política maneja los hilos de su economía y la política debe estar anclada en la moralidad. Por eso es particularmente romántico dedicarle el libro a los parados, "que merecen algo mejor".

El libro supone un paso más a los anteriores libros de economía post-crisis, muchos de los cuales hemos resumido en Know Square. Ese paso más es que, como el propio autor afirma, no se dedica a explicar cómo hemos llegado hasta aquí, sino cómo podemos salir.

Y lo hace resucitando las políticas keynesianas. En su opinión, Keynes es totalmente válido en situaciones económicas depresivas de trampa de liquidez. Krugman desafía el pensamiento convencional económico para afirmar las políticas neo-keynesianas. Su objetivo final, no obstante, no son los economistas, sino cambiar la opinión del público general.

Si hay algo que le sobra al libro son las menciones críticas a personas que difieren de su opinión. Basta con citar los argumentos, no hace falta generar animadversión al citar expresamente a los autores de dichos argumentos.

A pesar de todo, sus teorías resultan extraordinariamente atractivas y convincentes. De hecho, le dedica bastantes párrafos a analizar la situación española y europea, lo que constituye una importante novedad para un economista americano. No obstante, las políticas expansionistas fiscales que propone Krugman quizás sean más eficaces para Estados Unidos que para España. A la vista del despilfarro autonómico y estatal, darle más gasolina a la clase política es jugar a la ruleta rusa con el futuro.

Esto me recuerda a una metáfora que un ecologista empleó una vez y que es aplicable a nuestra situación: las medidas de impulso de demanda son como dar un puñetazo a una mesa con tal fuerza que vaya desplazando el vaso. Habrá un momento en el que el vaso acabe en el final de la mesa y un último puñetazo lo acabe sacando de la mesa. Vaso roto. En otras palabras, quizás impulsar la masa monetaria hasta el límite y practicar políticas expansivas pueda en algún momento gripar del todo el motor.

Estén los lectores de acuerdo o no, su lectura es obligada.

Resumen

"Leverage—rising debt compared with income or assets—feels good until it feels terrible".

"But banking is not like trucking, and the effect of deregulation was not so much to encourage efficiency as to encourage risk taking"

"You can’t have prosperity without a functioning financial system, but stabilizing the financial system doesn’t necessarily yield prosperity"

"It won’t be a tragedy if debt actually continues to grow, as long as it grows more slowly than the sum of inflation and economic growth"

"All debt isn’t created equal, which is why borrowing by some actors now can help cure problems created by excess borrowing by other actors in the past"

"No boom, no inflation"

"Compromise, if you must, on the policy—but never on the truth"

"The outstanding faults of the economic society in which we live are its failure to provide for full employment and its arbitrary and inequitable distribution of wealth and incomes" (Keynes)

"The boom, not the slump, is the time for austerity" (Keynes)

We need to take action to promote a full recovery. And we know how to do that. Too many people who matter (politicians, public officials, etc.) have, for a variety of reasons, chosen to forget the lessons of history and the conclusions of several generations’ worth of economic analysis, replacing that hard-won knowledge with ideologically and politically convenient prejudices.

Our objective should be making sure everyone has a job. We’re currently producing around a trillion dollars less of value each year than we could and should be producing.

The point is that the problem isn’t with the economic engine, which is as powerful as ever. Instead, we’re talking about what is basically a technical problem. Now, many people find this message fundamentally implausible, even offensive. It seems only natural to suppose that large problems must have large causes, that mass unemployment must be the result of something deeper than a mere muddle. We all know that sometimes a $100 battery replacement is all it takes to get a stalled $30,000 car back on the road.

We are suffering from a severe overall lack of demand. To understand this, let me tell you (again) my favourite story, the Capitol Hill babysitting co-op, an association of around 150 young couples, mainly congressional staffers, who saved money on babysitters by looking after each other’s children. They created a scrip system: couples who joined the co-op were issued twenty coupons, each corresponding to one half hour of babysitting time. (Upon leaving the co-op, they were expected to give the same number of coupons back.) Whenever babysitting took place, the babysittees would give the babysitters the appropriate number of coupons. This ensured that over time each couple would do as much babysitting as it received, because coupons surrendered in return for services would have to be replaced. Eventually, the co-op got into trouble: On average, couples would try to keep a reserve of babysitting coupons in their desk drawers, just in case they needed to go out several times in a row. But for reasons not worth getting into, there came a point at which the number of babysitting coupons in circulation was substantially less than the reserve the average couple wanted to keep on hand. In short, the babysitting co-op fell into a depression, which lasted until the economists in the group managed to persuade the board to increase the supply of coupons. What do we learn from this story? Your spending is my income, and my spending is your income. Three lessons about it:

1) First, we learn that an overall inadequate level of demand is indeed a real possibility.

2) Second, an economy really can be depressed thanks to magneto trouble, that is, thanks to failures of coordination rather than lack of productive capacity. Collectively, the world’s residents are trying to buy less stuff than they are capable of producing, to spend less than they earn.

3) Third, big economic problems can sometimes have simple, easy solutions. The co-op got out of its mess simply by printing up more coupons.

Well, the truth is that printing more babysitting coupons is the way we normally get out of recessions. But now increasing the monetary base is not working because we are in the unhappy condition known as a "liquidity trap".

The Fed can push interest rates down only so far. Specifically, it can’t push them below zero, because when rates get close to zero, just sitting on cash is a better option than lending money to other people. That’s the liquidity trap: it’s what happens when zero isn’t low enough, when the Fed has saturated the economy with liquidity to such an extent that there’s no cost to holding more cash, yet overall demand remains too low.

What we need to get out of this current depression is another burst of government spending. Is it really that simple? Would it really be that easy? Basically, yes.

The combination of the liquidity trap, and the overhang of excessive debt has landed us in a world of paradoxes, a world in which virtue is vice and prudence is folly.

In the 1960s macroeconomists shared a common view about what recessions were, and while they differed on the appropriate policies, these reflected practical disagreements, not a deep philosophical divide. Since then, however, macroeconomics has divided into two great factions: "saltwater" economists (mainly in coastal U.S. universities), who have a more or less Keynesian vision of what recessions are all about; and "freshwater" economists (mainly at inland schools), who consider that vision nonsense. "New Keynesian" theory found a home in schools like MIT, Harvard, and Princeton. And the result was that instead of being helpful when crisis struck, all too many economists waged religious war instead.

The world of paradoxes

Consider Minsky’s "financial instability hypothesis". Minsky’s big idea was to focus on leverage—on the buildup of debt relative to assets or income. Periods of economic stability, he argued, lead to rising leverage, because everyone becomes complacent about the risk that borrowers might not be able to repay. But this rise in leverage eventually leads to economic instability. Indeed, it prepares the ground for financial and economic crisis. Debt is a very useful thing. Debt is a way for those without good uses for their money right now to put that money to work, for a price, in the service of those who do have good uses for it.

The great American economist Irving Fisher laid out the paradox of deleveraging in a classic 1933 article titled "The Debt-Deflation Theory of Great Depressions": precautions that may be smart for individuals and firms—and indeed essential to return the economy to a normal state—nevertheless magnify the distress of the economy as a whole. If too many players in the economy find themselves in debt trouble at the same time, their collective efforts to get out of that trouble are self-defeating. "The more the debtors pay, the more they owe", or "debtors can’t spend, and creditors won’t spend". You can see this dynamic very clearly if you look at European governments.

Gauti Eggertsson explained the "paradox of flexibility": ordinarily, when you’re having trouble selling something, the solution is to cut the price. So it seems natural to suppose that the solution to mass unemployment is to cut wages. And today it’s often argued that more labor market "flexibility"—a euphemism for wage cuts—is what we really need. But an across-the-board cut in wages leaves everyone in the same place, except for one thing: it reduces everyone’s income.

Government borrowing

So what does government borrowing do? It gives some of those excess savings a place to go—and in the process expands overall demand, and hence GDP. It does NOT crowd out private spending, at least not until the excess supply of savings has been sopped up, which is the same thing as saying not until the economy has escaped from the liquidity trap. Our current problem is, in effect, a problem of excess worldwide savings, looking for someplace to go.

But what about Italy, Spain, Greece, and Ireland? As we’ll see, none of them is as deep in debt as Britain was for much of the twentieth century, or as Japan is now, yet they definitely are facing an attack from bond vigilantes. What’s the difference? Italy, Spain, Greece, and Ireland, by contrast, don’t even have their own currencies at this point, and their debts are in euros—which, it turns out, makes them highly vulnerable to panic attacks.

We won’t ever have to pay off the debt; all we’ll have to do is pay enough of the interest on the debt so that the debt grows significantly more slowly than the economy. One way to do this would be to pay enough interest so that the real value of the debt—its value adjusted for inflation—stays constant; this would mean that the ratio of debt to GDP would fall steadily as the economy grows. To do this, we’d have to pay the value of the debt multiplied by the real rate of interest—the interest rate minus inflation. And as it happens, the United States sells "inflation-protected securities" that automatically compensate for inflation.

Europe

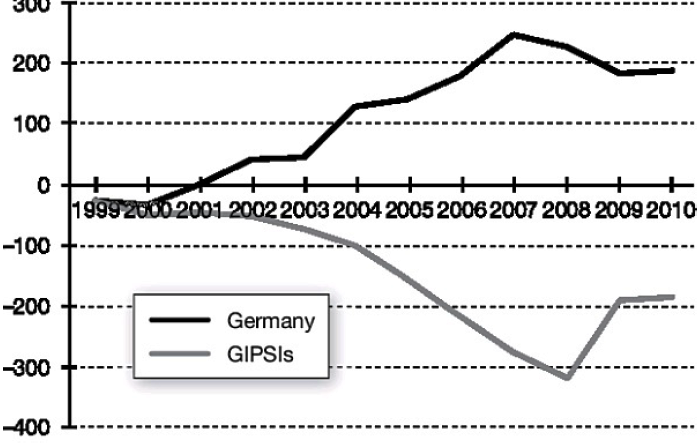

The euro made investors feel safe putting their money into countries that had previously been considered risky. Interest rates in southern Europe had historically been substantially higher than rates in Germany, because investors demanded a premium to compensate for the risk of devaluation and/or default. With the coming of the euro, those premiums collapsed: Spanish debt, Italian debt, and even Greek debt were treated as being almost as safe as German debt. This amounted to a big cut in the cost of borrowed money in southern Europe; it led to huge housing booms that quickly turned into huge housing bubbles. These inflows of capital fed booms that in turn led to rising wages: in the decade after the euro’s creation, unit labor costs (wages adjusted for productivity) rose about 35 percent in southern Europe, compared with a rise of only 9 percent in Germany.

Trade imbalances

Source: International Monetary Fund

And suddenly the euro found itself facing a huge asymmetrical shock, one that was made much worse by the absence of fiscal integration.

Wages are subject to "downward nominal rigidity," which is econospeak for the fact, overwhelmingly borne out by recent experience, that workers are very unwilling to accept explicit pay cuts. It is a big problem for some European nations, which badly need to cut their wages relative to wages in Germany. It’s a terrible problem, but one that would be made considerably less terrible if Europe had 3 or 4 percent inflation.

Other actions

Professor Bernanke argued that there were other measures monetary authorities could take that would be effective even with short-term rates up against the "zero lower bound." Among the measures were the following:

• Using newly printed money to buy "unconventional" assets like long-term bonds and private debts.

• Using newly printed money to pay for temporary tax cuts.

• Setting targets for long-term interest rates—for example, pledging to keep the interest rate on ten-year bonds below 2.5 percent for four or five years, if necessary by having the Fed buy these bonds.

• Intervening in the foreign exchange market to push the value of your currency down, strengthening the export sector.

• Setting a higher target for inflation, say 3 or 4 percent, for the next five or even ten years.

Unfortunately, Chairman Bernanke hasn’t followed Professor Bernanke’s advice. To be fair, the Fed has moved to some extent on the first bullet point above: under the deeply confusing name of "quantitative easing," it has bought both longer-term government debt and mortgage-backed securities.

Countering the present arguments

• "We need to focus on the long run, not the short run". This is wrong on multiple levels. Adjusted for inflation, public investment has fallen sharply since the slump began. Again, this means that if and when the economy finally does recover, we’ll run into bottlenecks and shortages far too soon.

• "We can’t expect a return to full employment anytime soon, because we need to transfer workers out of an overblown housing sector and retrain them for other jobs". But what we see instead is impoverishment all around, which is what happens when the economy suffers from inadequate demand.

• "We have fallen on hard times, and the remedy is a regime of virtue and prudence". This comes from Schumpeter and the liquidationist school. Even Milton Friedman had crusaded against this kind of thinking.

• "We are in this situation due to the government’s fault, not the banks". This is a big lie because the great bulk of risky lending was undertaken by private lenders. Freddie Mac did start buying subprime mortgages from loan originators late in the game, but it was clearly a follower, not a leader.

• "Fiscal stimulus is not effective". The Obama administration did in fact design and enact a stimulus bill, the American Recovery and Reinvestment Act. Unfortunately, the bill, clocking in at $787 billion, was far too small for the job. Almost 40 percent of the total consisted of tax cuts, which were probably only half or less as effective in stimulating demand as actual increases in government spending. So a realistic assessment was that the stimulus would have to deal with three or more years of severe economic pain. And the U.S. economy is really, really big, producing close to $15 trillion worth of goods and services every year. Think about that: if the U.S. economy was going to experience a three-year crisis, the stimulus was trying to rescue a $45 trillion economy. 787 billion does not seem much now, does it? What the work says, clearly and overwhelmingly, is that changes in government spending move output and employment in the same direction: spend more, and both real GDP and employment will rise; spend less, and both real GDP and employment will fall.

• "Excessive deficits will trigger the attack of the bond vigilantes". Much of the discussion in Washington had shifted from a focus on unemployment to a focus on debt and deficits. It is also false: between 2008 and 2011 the federal government borrowed more than $5 trillion. At the beginning of 2012 U.S. borrowing costs were close to an all-time low.

• "Cuts in government spending will lead to higher confidence and perhaps even to economic expansion". This argument is known as "expansionary austerity". Those who declare than down is up are called "Austerians", as the financial analyst Rob Parenteau felicitously dubbed them. Is it possible that cutting government spending can actually increase demand? Yes, it is. For instance, by reducing interest rates and/or by leading people to expect lower future taxes. But is not enough for these confidence-related effects to exist; they have to be strong enough to more than offset the direct, depressing effects of austerity right now. A decade before the crisis, back in 1998, the Harvard economist Alberto Alesina published a paper titled "Tales of Fiscal Adjustments". In that study he argued for strong confidence effects, so strong that in many cases austerity actually led to economic expansion. I fear those studies missed two points: the problem of spurious correlation, and the fact that fiscal policy usually isn’t the only game in town. Other studies demonstrate that fiscal austerity depresses the economy rather than expanding it.

• "Fiscal stimulus will create inflation". Austerity serves the interests of creditors, of those who lend as opposed to those who borrow and/or work for a living. Lenders want governments to make honoring their debts the highest priority; and they oppose any action on the monetary side that either deprives bankers of returns by keeping rates low or erodes the value of claims through inflation. But we are not seeing a rise in inflation. Why? Because of the liquidity trap. When you’re not in a liquidity trap, printing lots of money is indeed inflationary. But when you are in one, it isn’t; in fact, the amount of money the Fed prints is very nearly irrelevant. So when the Fed buys assets by crediting banks’ reserve accounts, the banks by and large just let the funds sit there:

• "If excessive debt brought us here, how, then, can even more debt be part of the appropriate policy response?" All debt isn’t created equal, which is why borrowing by some actors now can help cure problems created by excess borrowing by other actors in the past.

• "Europe’s crisis was essentially caused by fiscal irresponsibility". Countries ran excessive budget deficits, the story goes, getting themselves too deep into debt—and the important thing now is to impose rules that will keep this from ever happening again. This happened to Greece, but not other countries such as Spain. The essential Spanish problem, from which all else flows, is the need to get its costs and prices back in line. How can that happen? Suppose that the European Central Bank (ECB) followed an easy-money policy while the German government engaged in fiscal stimulus; this would mean full employment in Germany even as high unemployment persisted in Spain. So Spanish wages wouldn’t rise much if at all, while German wages would rise a lot; By the way, if you want an illustration of Milton Friedman’s point that it’s much easier to cut wages and prices by simply devaluing your currency, look at Iceland. Look at the three Scandinavian countries, Finland, Sweden, and Denmark, all of which should be considered highly creditworthy. Yet Finland, which is on the euro, has seen its borrowing costs rise substantially above those of Sweden, which has kept its own, freely floating currency, and even those of Denmark, which maintains a fixed exchange rate against the euro but retains its own currency and hence the potential to bail itself out in a cash squeeze. First, and most urgently, Europe needs to put a stop to panic attacks. One way or another, there has to be a guarantee of adequate liquidity. Second, those nations whose costs and prices are way out of line—the European countries that have been running large trade deficits, but can’t continue to do so—need a plausible path back to being competitive. To best solution is significant inflation in the surplus countries, and a somewhat lower but still significant inflation rate—say, 3 or 4 percent—for the euro area as a whole. Finally, although fiscal issues aren’t at the heart of the problem, the deficit countries do at this point have debt and deficit problems, and will have to practice considerable fiscal austerity over time to put their fiscal houses in order.

• "Bigger deficits would undermine confidence". There’s no reason to believe that even a substantial stimulus would undermine the willingness of investors to buy U.S. bonds.

• "Fiscal stimulus won’t work because there are no good projects in which to spend". This argument has more force. But still, it has been obvious from the beginning of this depression that the risks of doing too little are much bigger than the risks of doing too much. If government spending threatens to lead to an overheated economy, this is a problem the Federal Reserve can easily contain by raising interest rates a bit faster than it might have otherwise.

Conclusion

Compromise, if you must, on the policy—but never on the truth. Nothing Succeeds like Success. Real voters are busy with their jobs, their children, and their lives in general. What they notice, and vote on, is whether the economy is getting better or worse; statistical analyses say that the rate of economic growth in the three quarters or so before the election is by far the most important determinant of electoral outcomes.

All that is blocking recovery is a lack of intellectual clarity and political will.

TRANSPARENCY VOW

El autor de este resumen no conoce al autor ni tiene relación con la editorial ni con las instituciones ligadas al autor.

Adjunto