Saving the American Dream (Reseña del documento de Stuart Butler, Alison Acosta y William Beach)

Sus proyecciones son estáticas y hay poco soporte documental numérico, por lo que es difícil analizar la exactitud de sus propuestas. No obstante, son ideas que, como siempre, conviene tener en cuenta y que reflejan el actual debate sobre el estado de las cuentas públicas: reducir gasto para equilibrar la deuda futura o mantenerlo para impulsar el crecimiento. La reducción de las partidas de Sanidad se hace introduciendo al sistema público en el mercado, en competencia con la oferta privada.

Hay que destacar la veracidad indiscutible de un principio que hasta ahora se ha soslayado: la responsabilidad fiscal. Serán estas medidas u otras, pero debe implantarse más pronto o más tarde una limitación del déficit y por tanto una responsabilidad fiscal del Estado, tanto en Estados Unidos, como en los países europeos.

Se recomienda su lectura a interesados en economía o profesionales y directivos relacionados con las áreas de Sanidad e infraestructuras.

Resumen-crítica

The American dream is under threat by a national government overextended and unrestrained. We are being publicly lectured by the communist Chinese creditors. We are on the verge of becoming a country in decline: debt-bound, heavily regulated and bureaucratic, less self-governing and less free.

But we can turn the tide: we can get spending under control, balance the budget, and shrink our debt. We can limit the size of government and set free once again the unlimited genius of Americans to create wealth and jobs.

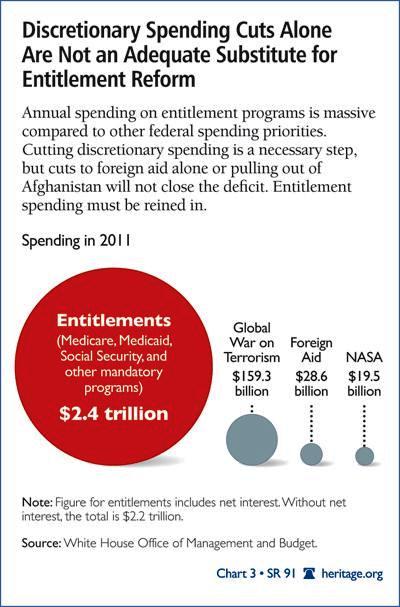

43% of total federal spending is accounted by Social Security, Medicare, Medicaid (10,3% GDP). We need to focus them on those who really need them.

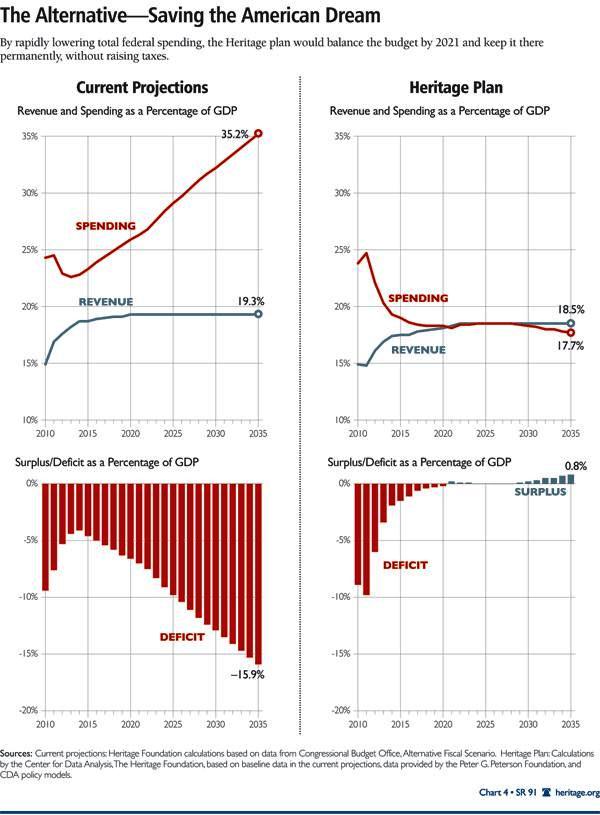

Saving the American Dream is our plan to fix the debt, cut spending and, above all, restore prosperity. It balances the nation’s budget within a decade—and keeps it balanced.

Our plan also encourages Americans to become more fiscally responsible. The plan has a higher moral purpose: we must not let the next generation and future ones pay punitive tax rates that will end liberty as we have known it.

There is only one real choice

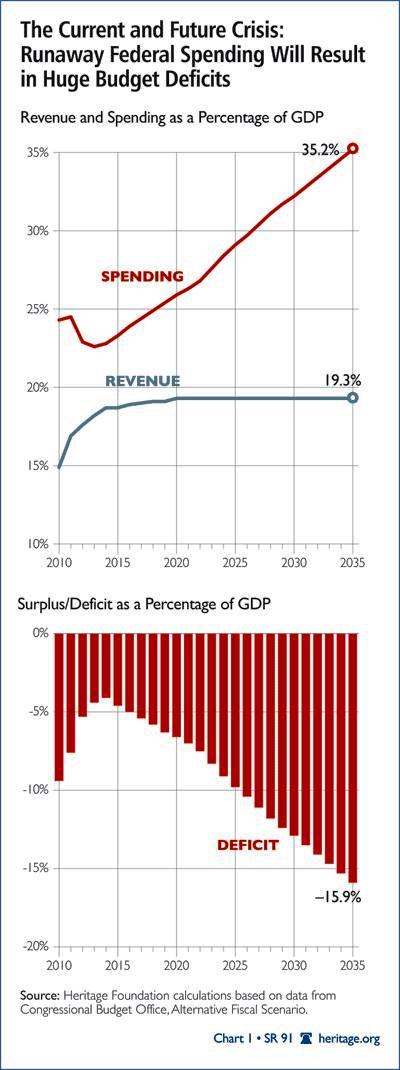

The government is doing things it should not be doing and spending far more than we can afford to pay or should be paying. Spending since World War II is at record levels as a proportion of the U.S. economy (in terms of gross domestic product, or GDP) and is growing.

The U.S. economy is already in worse shape than the stumbling economies of most European nations.

Washington promised expensive Medicare and Social Security benefits to the baby-boom generation, but the money to pay for these programs is running out. Fifty years ago, there were five workers paying the benefits of each retiree. Today, there are only three workers per retiree, and in 20 years, there will be just two.

Pay-as-you-go schemes can work only as long as enough people are paying into the system. Yet with the leading edge of the enormous baby-boom generation now reaching retirement, these programs are no longer cash cows covering other government spending.

There are three options:

• Choice #1 – Hope for the best

Each working American and each of his or her children now owes more than $200,000. The "easy-way-out" strategy is printing money to pay the bills, but it leads to rampant inflation. Global capital markets will demand action at some point.

• Choice #2: Raise taxes.

For instance, financing promised entitlement spending solely by raising tax rates would require doubling the marginal tax rates for all income brackets over the next 30 years, reaching a 66 percent federal income tax rate for many middle-income Americans.

• Choice #3: Actually fix the spending and debt problem and begin to restore the federal government to its proper functions.

This will mean deep and sustained reductions in federal spending. We must also hold down taxes while reforming our needlessly complex, burdensome, and highly unfair tax system to sharpen incentives and reward saving.

This choice requires that we tackle the root of the spending problem by squarely addressing the unsustainable entitlement promises that are overwhelming us.

The economic equation consists of two elements: reduce the crippling debt and foster the American spirit of self-reliance to flourish.

Proposals

Social Security

Social Security is the largest single federal program, paying out about $700 billion per year to some 60 million Americans. Yet Social Security went into the red in 2010, paying out more in benefits than people paid in as payroll taxes.

Social Security provides:

(1) Retirement income to workers and their spouses,

(2) Survivors benefits to the family members of deceased workers,

(3) Disability benefits for workers who have been injured and are unable to work and to the families of those workers.

The program is funded by a 12.4 percent payroll tax that is paid equally by both the worker (6.2 percent) and his or her employer (6.2 percent). Employers correctly see their contribution as a part of the employee’s total compensation.

Social Security will gradually be transformed from an "income replacement" system back to its original purpose of guaranteeing seniors freedom from fear of poverty and assuring a decent retirement income. This means that Social Security benefits will evolve over time into a flat payment to those who work more than 35 years—a flat payment that is sufficient to keep them out of poverty throughout their retirement.

Because the new Social Security is a real insurance system, designed to protect seniors from poverty, retirees with high incomes from sources other than Social Security will receive a smaller check, and very affluent seniors will receive no check.

To help make up the difference between the new Social Security benefit and what workers may desire for a more comfortable retirement, our plan will create greater incentives for workers of all income levels to save more for retirement. These savings will supplement their Social Security and create a more secure retirement.

For this reason, the Social Security retirement ages will be raised gradually and then indexed to life expectancy. This will create a more reasonable balance between the number of years a person works and the number of years one receives Social Security benefits.

To encourage people to stay in the workforce longer, those who work beyond full retirement age will receive a higher level of after-tax income during the period when they are not claiming benefits.

The flat benefit will be the equivalent of about $1,200 per month in 2010 dollars when the reform is complete. This is both higher than today’s average Social Security retirement benefit payment ($1,164 per month) and well above the 2009 poverty level for a single adult over age 65 ($857 per month).

Real insurance also protects seniors from poverty if their financial situation changes. Retirees who suffer a sudden and permanent drop in non–Social Security income would find their benefits rapidly restored.

Medicare

Medicare is the federal government’s health insurance program for all Americans age 65 and older and for the disabled. In 2010, the program covered 47 million enrollees.

• Basically, the Heritage plan introduces the powerful forces of consumer choice and competition into Medicare. The record shows that this approach can successfully control and slow the growth of health care costs while increasing patient satisfaction.

• All new retirees receive a contribution (premium support) from the government, just as federal employees and retirees do today. They can use this contribution to choose Medicare’s premium-based FFS plan or one of the other health plans.

• During the first five years of the premium-support program, the government’s contribution is based on the weighted average premium of the regional bids of competing health plans. After the first five years, the government contribution is based on the lowest bid of competing plans in a region.

• Low-income enrollees receive the full Medicare defined contribution.

• Enrollees with incomes over $110,000 and couples with incomes over $165,000 receive no government contribution and pay full, unsubsidized premiums.

• Like the Social Security adjustments in retirement age, Medicare’s eligibility age becomes 68 in 10 years and is indexed thereafter for increases in longevity.

• The Heritage plan also caps total Medicare spending. The spending cap is indexed annually for inflation using the Consumer Price Index plus 1 percent and Medicare population growth.

• The previous organizational and benefit distinctions within Medicare FFS (Medicare Parts A, B, C, and D) disappear because Medicare becomes a single, unified program with a unified trust fund that is financed by a defined contribution.

Health Care for families

Health care costs are rising at an alarming rate, while individuals and families have less control over their health care dollars or decisions. Worse still, the recently enacted Patient Protection and Affordable Care Act (PPACA, or Obamacare) is accelerating these problems. We propose the elimination of Obamacare and the creation of a health care system that fosters the individual choice, competition, and state-level innovation needed to control underlying health costs while assuring continuous and portable coverage. By overhauling subsidies and tax breaks for health care, we ensure that Americans can afford adequate coverage.

Under today’s system, the tax code provides unlimited tax breaks only to those workers who receive coverage through their employers. Workers cannot use this tax break if no plan is offered through their employers or if they simply prefer a plan other than their employer’s. Moreover, while upper-income workers obtain a very large tax break, the exclusion provides little or no help to lower-income workers who are struggling to afford coverage for their families.

• The Heritage plan ensures that everyone, regardless of job situation, is eligible for a tax credit or other help in purchasing health insurance. This means that people can buy, own, and keep the health care plans of their choice. We propose a nonrefundable fixed tax credit for households to purchase health coverage. The credit is phased out as income rises and eliminated for upper-income households.

• The Heritage plan ends the existing tax exclusion for employee compensation in the form of employer-sponsored health insurance. Employers and employees could decide whether to have the employer continue to buy coverage or to cash out the existing coverage in the form of higher cash income. Either way, the tax break for coverage would change from an exclusion to a credit. This credit can be used either to offset the cost of coverage offered through the workplace or to buy insurance outside the workplace.

• Medicaid, the federal–state program for the poor and the indigent, provides supplemental coverage for about 8 million Medicare beneficiaries. With the tax credit, Medicaid beneficiaries can enroll in private coverage.

• There is no mandate on individuals to obtain insurance, but if they did not obtain coverage, they would have to forgo the credit or assistance for insurance.

Additional Major Spending Reforms

Since 2000, non-defense discretionary outlays have expanded 50 percent faster than inflation. Antipoverty spending has risen 83 percent faster than inflation, and other programs have grown rapidly. Despite multiple government audits that have shown many programs to be duplicative or ineffective, no significant federal program has been eliminated in more than a decade. Government continues to grow, financed by taxes on Americans and an explosion of borrowing that is imposing huge additional burdens on future generations.

• Returning most Non-Defense Discretionary Spending to 2008 Levels, non-defense discretionary spending accounts for 4.5 percent of GDP—is reduced to 2.0 percent of GDP by 2021.

• In addition, antipoverty spending is reformed. Obamacare is repealed, as noted earlier, and replaced with an alternative solution to uninsurance and high costs.

• With improvements in efficiency, we estimate that defense needs will require spending approximately 4 percent of GDP for the foreseeable future.

• The federal government should focus on performing a limited number of appropriate governmental duties well while empowering state and local governments, which are closer to the people, to address local needs creatively in such areas as transportation, justice, job training, the environment, and economic development. Freezing this spending at 2008 levels through 2015 and then capping subsequent growth at the inflation rate would save more than $2 trillion in the first decade and even more thereafter.

• The President’s costly high-speed rail program is terminated.

• Finally, all non-safety functions of the Federal Aviation Administration (FAA) are transferred to the private sector, and most FAA fees are eliminated. The air traffic control system will be transferred to the private sector, where it belongs, and financed by flight ticket user fees. The airport improvement program is also terminated, with airlines, state government, and private investment taking the place of the federal taxpayer.

• Scaling Back K–12 Education Spending and Reforming Higher Education Spending.

• The war on terrorism has increased defense spending to approximately 5 percent of GDP, yet it remains well below the 9 percent spent during in the 1960s and the 6 percent spent during the 1980s. While the Heritage plan recognizes that predicting precise funding requirements for overseas contingency operations is impossible, it is reasonable to expect that the phasedown in those efforts will permit reducing defense spending to approximately 4 percent of GDP and maintaining it at that level.

• Replacing Farm Subsidies with Farmer Savings Accounts. Intended to remedy low crop prices and farmer poverty, the current farm subsidy system does neither. Farm subsidies encourage overplanting, which drives prices down further, necessitating even more subsidies. Moreover, rather than focusing on low-income farmers, most farm subsidies go to commercial farmers who report an average annual income of nearly $200,000.

• Asset Sales. Sales of assets would immediately reduce the government’s operating deficit and debt, reducing future interest costs.

• Reforming the Federal Budget Process. We change the budget process to impose enforceable caps to reduce total federal spending to 18.5 percent of GDP by 2021 (including entitlement programs) and then keep spending at that level.

• We also cap non-defense discretionary spending at 2.0 percent of GDP.

• To make the budget process more visible, understandable, and accountable to the American people, we require Congress to estimate and publish the projected cost over 75 years of any proposed policy or funding level for each significant federal program.

Tax Reform

A simple, transparent tax is needed so that taxpayers can anticipate and plan for the tax consequences of their actions and easily understand the full extent of their tax burden. It also provides greater confidence that other taxpayers are not exploiting tax complexities to underpay their taxes. It will not impose multiple levels of taxation on saved income.

The tax will collect revenues equivalent to 18.5 percent of the economy. The modern average of tax revenue under normal economic conditions is approximately 18.5 percent of GDP. This is the upper limit that Americans have over many decades indicated to politicians they are prepared to accept. Thus, the tax system should be capped at collecting no more than this amount both to ensure a strong economy and to restrain the growth of government.

NOTA KNOW SQUARE – Dependerá de la productividad. A mayor productividad, más impuestos habrá que pagar por americano…

• A Unified Single Tax Rate: applied to income after deducting all savings.

• Savings will be taxable only when spent.

• This eliminates the current-law bias against saving and ensures that individuals pay taxes only on what they withdraw from the economy and not on savings that they make available for investment in the economy by others.

• Today’s business tax code will be replaced by a flat business tax on domestic sales of goods and services with deductions for labor costs and purchases from other businesses, including expensing of capital purchases. All business activity, including corporate, will be taxed under the new flat business tax.

• Elimination of the death tax.

• The statutory individual and business tax rate will likely eventually be between 25 percent and about 28 percent under traditional scoring methods.

• The more individuals or families save, the lower their taxes; they pay tax on savings only when savings are used to pay for goods and services.

• However, the new tax system does not tax government transfers explicitly associated with low-income citizens, such as welfare, health care assistance, and similar programs.

• By 2021, total tax savings will exceed $3.1 trillion.

TRANSPARENCY VOW

El autor de este resumen no conoce a los autores individuales ni a las Fundaciones para las cuales trabajan.

Sobre el autor

La "Heritage Foundation" es un think tank americano fundado en 1973 con el objetivo de promover políticas públicas conservadoras y basado en la libre empresa, el rol reducido del gobierno, la libertad individual y los "valores tradicionales americanos".

El documento está patrocinado por la Peter G. Peterson Foundation, una fundación fundada en 2008 con activos de mil millones de dólares donados por el político y banquero Peterson. El objetivo de esta Fundación es la de generar atención pública sobre la sostenibilidad fiscal americana.

Título del documento

"Saving the American Dream: The Heritage Plan to Fix the Debt, Cut Spending, and Restore Prosperity"

Editorial: Heritage Foundation

Autores: Stuart Butler, Ph.D., Alison Acosta Fraser and William Beach

1ª edición: Mayo 2011

53 páginas

Precio: gratuito

Versión digital en inglés.